What to Watch: The PBM Handoff

The issue is not whether PBMs face scrutiny. They already do. The question is whether settlements that look like closure become the map for the next legal attack.

Markets love a settlement.

It turns fog into a number. It gives analysts something to model, investors something to stop worrying about, and management something to call “behind us” on the next earnings call.

That is the current narrative on the latest pharmacy benefit manager settlements.

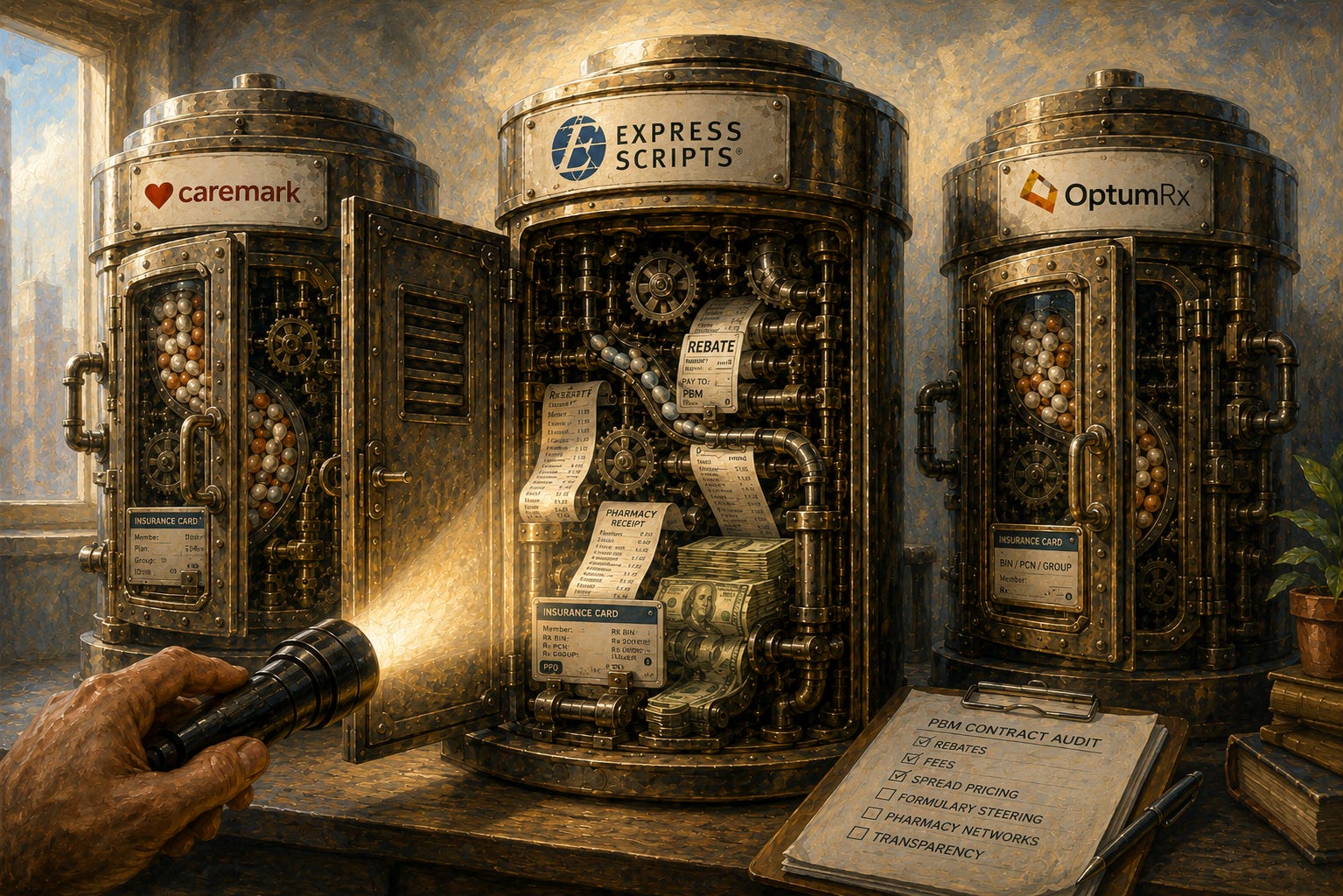

Express Scripts has settled with the FTC over insulin pricing allegations. CVS Caremark has reached a proposed settlement. OptumRx has moved toward one as well. For investors, that can look like the big Pharmacy Benefit Manager (PBM) legal cloud finally starting to break.

Maybe it is.

Or maybe the storm just found a new route.

A settlement can end one case while making the next one easier to bring. It can show later plaintiffs what conduct mattered, what documents to ask for, what remedies regulators accepted, and where the money moved.

That is the underrated PBM risk now.

The market may be treating settlement as closure. States, employers, private plaintiffs, and a future administration may treat it as a handoff.

What to Watch

First, watch whether PBM scrutiny moves from Washington headlines into employer contracts, state subpoenas, ERISA lawsuits, and pharmacy ownership fights.

That is where the risk starts to look less like politics and more like money.

The first FTC case was about insulin, but the larger question is not limited to insulin. It is whether the same pressure points can be used against the broader PBM model.

That is what makes PBMs hard to value from the outside.

The money does not move in one simple line. It moves through rebates, fees, spreads, reimbursement rates, pharmacy networks, specialty dispensing, mail-order volume, audit rights, and contract language that most patients and investors never see.

Opacity is not a side issue.

It is the machine.

That does not mean every PBM practice is illegal. Nor does it mean the companies cannot defend themselves. It does mean investors should be careful about treating the FTC settlements as the end of the story.

The better question is whether the settlements make the PBM business easier for others to attack.

How To Read This

The mistake is asking only whether CVS, Cigna, or UnitedHealth can absorb a settlement.

They probably can.

These companies are not fragile because of one check. The real question is whether PBM earnings deserve the same value if employers, states, and regulators start forcing more of the business into the open.

That is the difference between a fine and a business-model problem.

A fine is paid once. A business-model problem changes future contracts. It can change how rebates are passed through, how fees are disclosed, how pharmacies are reimbursed, how patients are steered, and how employers negotiate.

That is why the next stage matters.